Updated: Nov 28

To explain what we mean, here’s everybody’s favourite thing – a surprise maths test:

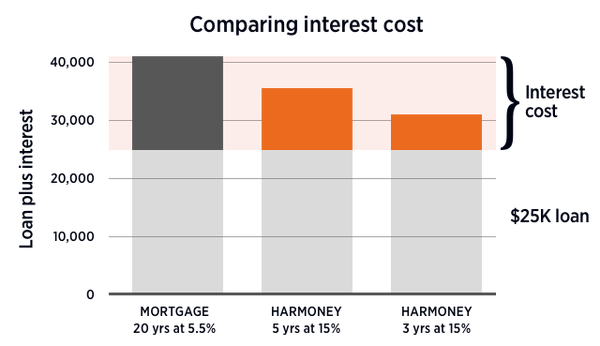

Say you need to borrow $25,000. You have the choice of borrowing that amount at:

A: 5.5% over 20 years

OR

B: 15% over 3 years

Which do you think is cheaper?

At first glance, it’s easy to assume the lower interest rate over the longer period would be the better deal. Rolling that extra $25,000 into your existing mortgage might seem pretty tempting.

But here’s the reality:

Borrowing $25,000 at 5.5% over 20 years, with monthly repayments, means you’ll pay a total of $41,273 – that’s $16,273 in interest alone.

Compare that to borrowing $25,000 at 15% over three years, also with monthly repayments. You’ll pay back a total of $31,199, or $6,199 in interest.

That’s almost $10,000 less.

Of course, we know interest isn’t everything. Different loans, different terms, and different repayment schedules will all affect the outcome. And another important factor is how much you can afford to repay each week.

For some people, rolling extra finance into their mortgage makes sense. It’s simple – one payment to manage. We get it. In fact, we’re big fans of debt consolidation here at Harmoney.

Many people promise themselves they’ll be super-disciplined and repay the extra amount within three or five years to save on interest. But sometimes, that’s easier said than done. Once the loan is folded into your mortgage, it’s harder to see the true cost of that extra debt – and easier to slip back into paying just the minimum each week or month.

If you’re thinking of transferring a personal loan to your mortgage, we’d suggest doing some maths homework first – to make sure it really is the best financial decision.

The good people at Sorted have excellent loan and mortgage calculators that can help you compare how much you’ll repay overall – and how much of that will be interest.

Here are a few more things to consider:

-

Is your mortgage rate fixed or floating? This can affect your total repayments.

-

Will your bank charge fees for refinancing your mortgage?

-

What can you realistically afford to repay, and how long do you want the debt to hang around?

Remember: it’s the interest cost that counts – not just the interest rate.