Interest rates and fees — archived November 2019

Note: this page was updated in November 2019. See current version. See previous version.

At Harmoney, we’re 100% open and transparent about our rates and fees. If you're thinking about getting a personal loan you can check what interest rate will apply to you through our 100% accurate, online quote. You won't be charged an Establishment Fee until your loan is funded. If you're a lender, you'll find details regarding the service fee below.

Interest rates

Harmoney's interest rates are priced on a risk gradient. Each loan application is attributed a risk grade with an associated interest rate according to Harmoney's credit scorecard. The interest rate on a loan is both the interest rate paid by borrowers and the gross interest rate due to Lenders. Harmoney's risk grades and their corresponding interest rates are displayed in the table below.

- During the loan application, borrowers provide us with some financial information;

- Based on an assessment of this information and the borrower's repayment history, we’ll assign a risk grade to the borrower;

- The borrower will then be able to apply for a loan at the interest rate that corresponds to their risk grade.

| Grade | Interest Rate (p.a.) |

|---|---|

| A1 | 6.99% |

| A2 | 7.99% |

| A3 | 9.20% |

| A4 | 10.50% |

| A5 | 11.99% |

| Grade | Interest Rate (p.a.) |

|---|---|

| B1 | 13.39% |

| B2 | 14.75% |

| B3 | 15.80% |

| B4 | 16.99% |

| B5 | 17.80% |

| Grade | Interest Rate (p.a.) |

|---|---|

| C1 | 18.90% |

| C2 | 20.40% |

| C3 | 21.90% |

| C4 | 22.99% |

| C5 | 23.99% |

| Grade | Interest Rate (p.a.) |

|---|---|

| D1 | 24.70% |

| D2 | 25.20% |

| D3 | 25.49% |

| D4 | 25.99% |

| D5 | 26.49% |

| Grade | Interest Rate (p.a.) |

|---|---|

| E1 | 26.99% |

| E2 | 27.49 |

| E3 | 27.99% |

| E4 | 28.29% |

| E5 | 28.69% |

| Grade | Interest Rate (p.a.) |

|---|---|

| F1 | 28.99% |

| F2 | 29.19% |

| F3 | 29.49% |

| F4 | 29.69% |

| F5 | 29.99% |

Interest rates effective from 7 November, 2019. Interest rates are subject to change.

Borrowing limits

Borrowers in Harmoney's marketplace are limited in the amount they can borrow, based on the credit grade they are assigned, and whether the loan is new or a rewrite (a rewrite loan is a "Top Up" of an existing loan). The following table shows these limits:

| Grade | Limits for new | Limits for rewrite |

|---|---|---|

| A1 ‑ A5 | $70,000 | $70,000 |

| B1 ‑ B5 | $50,000 | $50,000 |

| C1 ‑ C5 | $45,000 | $45,000 |

| D1 ‑ D5 | $35,000 | $35,000 |

| E1 ‑ E5 | $25,000 | $25,000 |

| F1 ‑ F5 | $15,000 | $15,000 |

Note: After final assessment Harmoney may, in its discretion, specify different ranges of maximum Loan Amounts which you are approved to list for.

Cost of borrowing

Using the links below, you can download a detailed spreadsheet showing the total cost of borrowing for a range of example loans. The spreadsheet includes 3 and 5 year terms for loan grades A1 - F5.

Loan calculator

For a quick estimate of how much money you can borrow and what your repayments will be like you can use our personal loan calculator

Borrower fees

Establishment Fee

Harmoney charges borrowers an up-front, one-off Establishment Fee of $200 for loans of below $5,000, or $450 for loans of $5,000 and above. The Establishment Fee is added to the approved loan amount.

The Establishment Fee will be charged on the loan being advanced. These Establishment Fees also apply to Top Ups.

Dishonour Fee

In the case where a orrower’s repayment is dishonoured, a $15 fee will be charged to the borrower’s account due to the additional administration required to re-process the payment. The fee will be due in the borrower's next payment.

Overdue Fee

The Overdue fee is charged if a payment is not made in full and the account goes into arrears. The fee payable is $20 on each of 6, 36, 66, 96, 120 days after the payment date, if the account remains outstanding. The fee will be payable on the borrower's next direct debit date.

Legal Fees

If enforcement action is required against a borrower, any legal and associated third party costs incurred will be charged to the borrower account. The costs charged are due in the borrower's next payment.

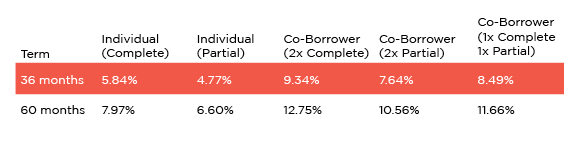

Payment Protect Fees (borrowers only)

If borrowers choose to add Payment Protect as an add-on to their loan, the Payment Protect fee will be added to their loan total and included in their monthly repayments. The Payment Protect fee is calculated as a percentage of the loan amount (including Establishment Fee), rounded to the nearest $25.

There are two levels of pricing based on the level of cover borrowers require or are eligible for:

| Cover | Included coverage |

|---|---|

| Partial | Terminal illness and death. |

| Complete | Death, terminal illness, disability illness and involuntary redundancy. |

If Payment Protect is taken out on a joint application, it must be taken out by both the primary borrower and the co-borrower; it cannot be taken out by only one party.

| Term | 36 months | 60 months |

|---|---|---|

| Individual (Complete) | 7.24% | 9.88% |

| Individual (Partial) | 5.92% | 8.18% |

| Co-Borrower (2x Complete) | 9.34% | 12.75% |

| Co-Borrower (2x Partial) | 7.64% | 10.56% |

| Co-Borrower (1x Complete 1x Partial) | 8.49% | 11.66% |

Note: Prices were changed on 15th August 2016. Click here to see old pricing.

{kind=link}

Rebate of fee on early repayment

If a borrower prepays their loan in full before the end of their originally set term, without having any payments waived, the Payment Protect fee is rebated pro rata using a formula prescribed by the Credit Contracts and Consumer Finance Act (CCCFA):

Payment Protect refund = ( p × s × ( s + 1)) ÷ ( t × ( t + 1))

Where:

- "p" is the Payment Protect fee amount,

- "s" is the number of whole months in the unexpired portion of the period for which the plan applied,

- and "t" is the number of whole months for which the plan applied.